Investor enthusiasm for the Zomato IPO (initial public offering) -- the first foodtech startup listing in India -- is palpable as the food services platform's IPO opens for subscription on Wednesday.

On Tuesday, the company's anchor book saw a strong response from global and domestic institutional investors, with the foodtech unicorn raising Rs 4196.5 crore, or about 45 percent of its total issue size, from 186 anchor investors, including marquee global names like Tiger Global, New World Fund, and Fidelity and domestic mutual funds like HDFC, SBI, and Axis.

Zomato said it finalised the allocation of 552.2 million shares to anchor investors at Rs 76 per share, the upper end of its Rs 72-76 IPO price band. The allotment of shares to anchor investors, which is done a day before the IPO, serves as an indication of the quality of and level of demand for the issue.

Indeed, while noting the general enthusiasm around the Zomato IPO, analysts at at least six brokerages, including Angel Broking and ICICI Direct Research, recommended investors ‘subscribe’ or 'subscribe for listing gains' to Zomato’s Rs 9,375 crore IPO, which opens for subscription on Wednesday, July 12 and closes on Friday, July 14.

"Zomato has been able to reduce its losses in FY21 despite a degrowth in topline (due to Covid-19). We expect losses to reduce further over the next couple of years due to rebound in growth and improving unit economic," predicts Angel Broking equity strategist Jyoti Roy.

"Given strong delivery network, high barriers to entry, expected turnaround and significant growth opportunities in tier-II and tier-III cities, we believe Zomato will command a premium to global peers and hence have a ‘subscribe’ recommendation on the IPO," Jyoti adds.

Zomato’s Rs 9,375 crore IPO comprises Rs 9,000 crore worth of fresh issue of equity shares and Rs 375 crore of secondary share sale by InfoEdge. The company is eyeing a post-issue valuation of Rs 64,365 crore.

New World Fund (3.91 percent), Tiger Global (3.87 percent), Morgan Stanley Asia (Singapore) Pte (3.43 percent), Canada Pension Plan Investment Board (2.99 percent), Ballie Gifford Pacific Fund (2.99 percent), Morgan Stanley Investment Funds Asia Opportunity Fund (2.74 percent), Fidelity Funds India Focus Fund (2.54 percent), Government of Singapore (2.30 percent), and Kotak Flexicap Fund (2.17 percent) were allotted more than two percent of the anchor investor portion.

Of the total allocation of 552.2 million shares to anchor investors, 184.1 million shares were allocated to domestic mutual funds through a total of 74 schemes, the company said.

First meaningful Internet IPO

The strong response Zomato has received from global and domestic institutional investors for its anchor book highlights the excitement around the first public listing of a tech startup that offers investors the potential to play India’s digital opportunity.

“Zomato IPO would mark the first meaningful Internet listing in India...which would allow investors to play the Internet theme. While the evolving business models are a risk to traditional consumer businesses, investor preference for the high growth Internet stocks may drive de-rating of traditional stocks including FMCG, retail etc,” says Jefferies analyst Vivek Maheshwari.

Analysts, however, cite concerns over Zomato's "sky-high valuation" and the likelihood of mounting costs over time as the company is expected to continue investing in growing its business.

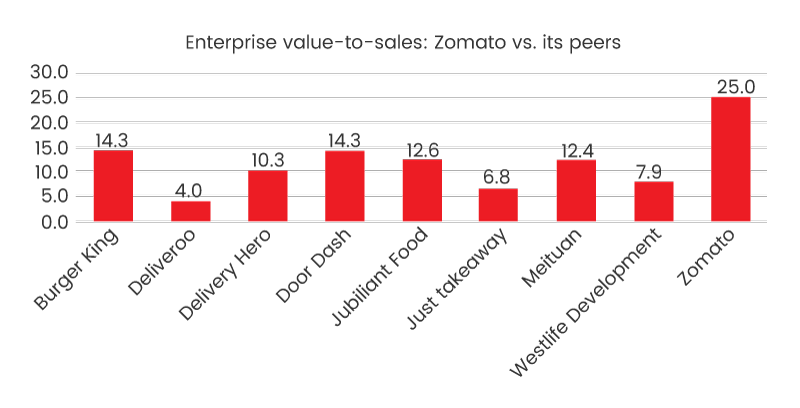

"Priced at FY20 EV/sales of 17.9x at upper price band Zomato is yet to turn profitable. However, this new-age digital platform offers strong growth potential, which at present is evolving on the back of favourable macroeconomics, changing demographic profile, rising adoption of tech infrastructure. Hence, we recommend subscribe to this IPO," urges ICICI Direct Research analyst Rashesh Shah.

ALSO READ

Over the past 12 years, Zomato has evolved to become a category leader in the foodtech industry, seizing the large opportunity in India's highly undepenetrated food services market.

The company has two core business-to-consumer (B2C) offerings: food delivery and dining-out. This is in addition to its business-to-business (B2B) offering, Hyperpure, as well as its paid membership programme business Zomato Pro, which encompasses both food delivery and dining-out.

Revenue contribution from its food delivery business has seen significant growth in the past five years alone, increasing to more than 80 percent in FY20, from about 55 percent in FY18 and almost nil in FY15. Delivery orders, meanwhile, also surged 13X to over 400 million in FY20 from 31 million in FY18, while gross order value (GOV) increased more than 8X in FY20 from FY18 levels.

Deepinder Goyal, co-founder and CEO, Zomato

"We are long-term constructive on the fortunes of Zomato. The industry structure is likely to remain a duopoly of Zomato and Swiggy with limited disruptions from the likes of Amazon and direct ordering companies like DotPe and Thrive. Coupled with the moats of network effects, branding, last-mile delivery, customer user behaviour (convenience and addiction) and wide geographical reach, we believe the duopoly is likely to dominate in the visible future," write analysts at Ventura.

They expect Zomato’s revenue to grow at a compound annual growth rate of 64.7 percent to Rs 8,910 crore by FY24 from Rs 1,994 crore in FY21, driven by an estimated 65.1 percent CAGR in food delivery business to Rs 7,722 crore, 68.5 percent CAGR in Hyperpure to Rs 958 crore, and 43.6 percent CAGR in platform services to Rs 231 crore.

Despite Zomato's "optically demanding" valuation of 5.1X FY24 enterprise value/sales, analysts at Ventura recommend investors subscribe for listing gains on account of the "...duopoly market, immense upside penetration potential, the humungous untapped online opportunity of the adjacent verticals, and scarcity premium."

ALSO READ

Room to grow in an underpenetrated market

For the past four years, Zomato has been consistently gaining market share in terms of GOV to become one of the largest foodservice players in India that operate in India’s largest hyperlocal delivery network.

As of March 31, 2021, Zomato had 389,932 active restaurant listings and a presence in 525 cities in India and 23 countries outside India.

For the FY18-FY21 period, Zomato's revenues also grew at a compound annual growth rate of 62.3 percent to Rs 1,994 crore, driven by 54.5 percent CAGR in food delivery business to Rs 1,716 crore, 266.7 percent two-year-CAGR in Hyperpure to Rs 200 crore, and 318.5 percent CAGR in platform services to Rs 78 crore.

Analysts note that Zomato operates in a highly underpenetrated market in India where, of the total food consumption, only 8-9 percent is from restaurants, of which only 8 percent is online food delivery. In comparison, in markets like the US and China, the restaurant food/online food delivery matrix stands at 40-50 percent each, thus suggesting a significant opportunity for Zomato to grow in the sector.

"Going forward, food services in India will gain share from the unorganised market and growth will be driven by changing consumer behaviour, reduced dependence on home-cooked food/kitchen set-up, increasing consumer disposable income and spending, and higher adoption among the smaller cities. Given the large market opportunity in India, we believe Zomato will focus on growing in Indian markets which will enhance the value for all stakeholders," says Religare Broking's Nirvi Ashar.

Nirvi, however, recommends investors consider subscribing for listing gains, over concerns the company is still loss-making, despite losses narrowing on a year-over-year basis and Zomato's strong growth plans that are expected to further boost its financial performance, going forward.

Still, analysts agree that investor buzz around the Zomato IPO is "tremendous" given it is the first startup in the Indian foodtech space to list on the bourses and operates in a highly underpenetrated, duopoly market with strong entry barriers.

"Zomato with first-mover advantage is placed in a sweet spot as the online food delivery market is at the cusp of evolution. The valuation also appears expensive... though valuing such early-stage businesses on plain vanilla financial matrix might not give the right picture. Investors with high-risk appetite can subscribe for listing gains given fancy for unique and first-of-its-kind listing in the food delivery business," adds Motilal Oswal Securities analyst Sneha Poddar.

Kotak Mahindra Capital company, Morgan Stanley India Company Pvt Ltd, and Credit Suisse Securities (India) Pvt Ltd are the global coordinators and book running lead managers to the issue. BofA Securities India Ltd and Citigroup Global Markets India Pvt Ltd have been appointed as merchant bankers to the public issue. The shares the company will be listed on BSE and NSE.

ALSO READ

Link : https://yourstory.com/2021/07/zomato-ipo-anchor-investors-response-analysts-recommend-subscribe

Author :- Tenzin Pema ( )

July 14, 2021 at 03:13AM

YourStory