The history of the Goods and Services Tax (GST) dates back to the year 2000 when the idea was suggested and stretched to 2017 when it was implemented with four bills relating to it becoming The Central Goods and Services Act.

The GST Act was introduced with the objectives to streamline and unify indirect taxes for goods and services across India by doing away with multiple indirect taxes levied by the central government and state governments/union territories, with the focus on "One Nation - One Tax market."

In the indirect tax regime before GST, each state collected Value Added Tax (VAT) for the sale of goods within the same state and the inter-state sale of goods, CST (Central State Tax) was levied by the centre. Service Tax was applicable for the sale of services and it was levied by the central government. GST has subsumed the following indirect taxes, including the above, prevalent before the inception of GST.

- Central Excise Duty, Duties of Excise, Additional Duties of Excise, Additional Duties of Customs, Special Additional Duty of Customs

- Cess, State VAT, Central Sales Tax, Purchase Tax

- Luxury Tax, Entertainment Tax

- Entry Tax

- Taxes on advertisements, Taxes on lotteries, betting, and gambling

The GST structure has mitigated the cascading effect of pre-GST indirect taxes to a great extent, thus making Indian products and services competitive in the domestic and international markets.

GSTN and GSTIN

GSTIN is a tax registration number under GST that businesses get after successful registration, whereas, GSTN aka the Goods and Services Network, is an organisation that manages the entire information technology (IT) system of the GST portal.

Input Tax Credit (ITC) under GST

The introduction of GST has helped in the reduction of the cost for end consumers. Under the old indirect tax regime, the tax liability was passed on to every next stage, and the final price effect came on the end consumer. This condition is known as the cascading effect.

Under the GST, businesses are allowed to set off the taxes they pay when they purchase any raw material, goods or service through the Input Credit Tax (ITC) method.

The effect of input tax credit reduces the final value of the goods under GST. Input tax credit under GST means, reducing the taxes paid on purchases (inputs) from the taxes to be paid on sales (output).

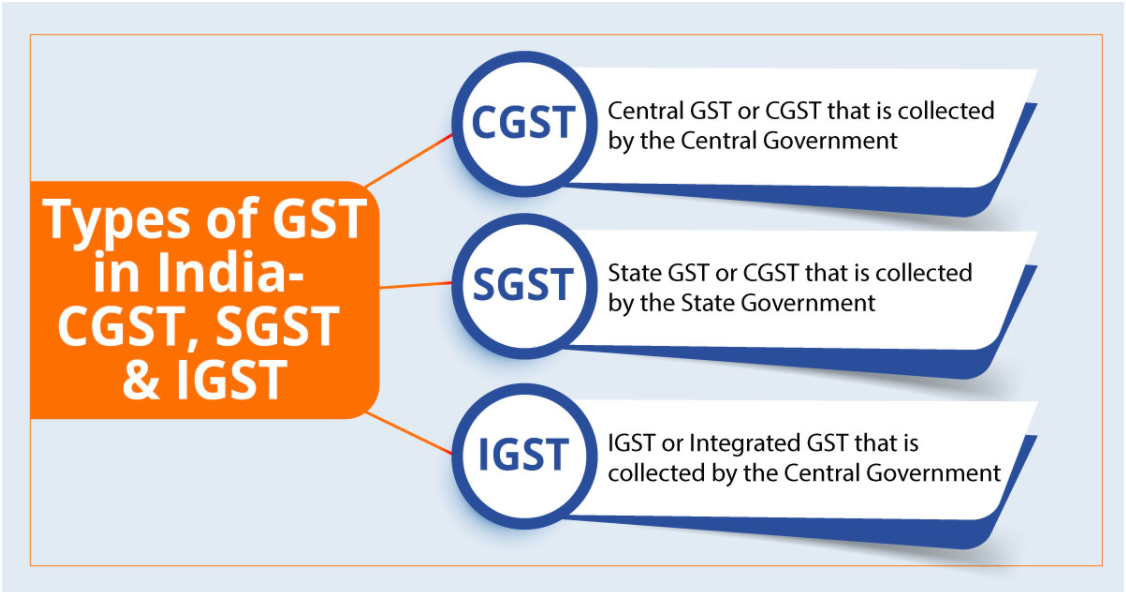

The components of GST

There are three taxes applicable under this system are:

- CGST: It is the tax collected by the central government on an intra-state sale (for example, a transaction happening within a state)

- SGST: It is the tax collected by the state government on an intra-state sale (for example, a transaction happening within a state)

- IGST: It is a tax collected by the central government for an inter-state sale (for example, between two states)

Multi-stage taxation structure

A product goes through multiple stages before it is consumed by the end-user. These stages are similar to those of a supply chain.

A typical supply chain of a product involves the following stages:

- Purchase of raw materials

- Manufacturing of a product

- Warehousing of a product

- Selling the product to a wholesaler and then to a retailer

- Sale to the end consumer

GST is levied on each stage mentioned above, which makes it a multi-stage tax.

Image Source: Shutterstock

Destination-based tax

While the previous indirect taxes were levied at the point of origin, GST is levied at the point of consumption of the goods or services. For instance, if a product is manufactured in West Bengal and is sold to an end consumer in Karnataka, then GST will be levied and collected by the Government of Karnataka and not West Bengal. It was the opposite under the old system.

GST tax slabs

GST consists of the following tax slabs – 0 percent, 5 percent, 12 percent, 18 percent, and 28 percent, with the majority of goods and services coming under the 18 percent bracket.

Certain products and services like petroleum products, high-speed diesel, motor spirit, natural gas, aviation turbine fuel, and alcoholic liquor for human consumption do not come under GST. These products and services are taxed by the central government individual state governments, under CST and VAT.

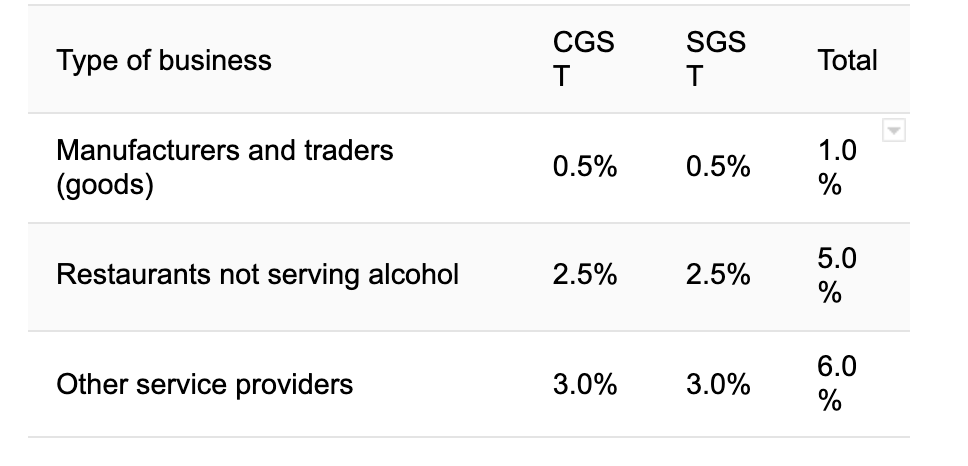

GST composition scheme

The composition scheme under GST allows taxpayers to enjoy a certain amount of flexibility when paying their taxes.

The scheme is ideal for SME and startup businesses with a turnover of less than Rs 1.5 crore. In the case of northeastern states and Himachal Pradesh, the threshold is Rs 75 lakh. Small taxpayers can only pay GST at a fixed rate of turnover.

The GST rates applicable to composition dealers are as follows:

There are many advantages to availing of the composition scheme, particularly for MSMEs and startups under this scheme, input credit cannot be availed. Some of these include the following:

- With the composition scheme, the government has ensured that more startups can flourish in a market that has become friendlier towards their plight.

- Businesses can also enjoy much higher liquidity as their taxes are set at a lower rate.

- Businesses can gain from lesser compliance that comes with all of these exemptions (maintaining records, filing returns, issuance of invoices, and so on), making it easier for them to run their operations.

Reverse Charge Mechanism (RCM) under GST

The government has clearly spelt out a few instances in which the reverse charge mechanism where the receiver of the goods becomes liable to pay tax is employed. Understanding the same can help both businesses and individual customers.

The RCM is applicable in instances like:

- A registered dealer buying goods or services from unregistered dealers,

- Ecommerce provider selling services,

- Supply of certain goods and services specified by CBIC (Central Board of Indirect Taxes and Customs)

GST council

The GST council is the key decision-making body that will take all important decisions regarding the GST. The GST council dictates tax rate, tax exemption, the due date of forms, tax laws, and tax deadlines, keeping in mind the special rates, and provisions for some states.

The council is headed by the Union Finance Minister, with the finance minister of all the states of India as members of the council.

GST HSN and SAC codes

HSN code means Harmonised System of Nomenclature code used for classifying the goods under the GST and the SAC Code means Services Accounting Code, under which services falling under GST are classified in India.

The Ministry of Finance has announced that businesses with a turnover of Rs 5 crore and above will have to furnish a six-digit HSN or tariff code on the invoices issued from April 1. Those with a turnover of up to Rs 5 crore in the preceding financial year would also be required to furnish a four-digit HSN code on B2B invoices.

GST registration

Businesses are required to register for GST if they fall into one of the following criteria as per the current rules.

Aggregate turnover: Any service provider who provides an aggregate service value of more than Rs 20 lakh in a year is required to obtain GST registration. (In the special category states, this limit is Rs 10 lakh). Any entity engaged in the exclusive supply of goods whose aggregate turnover crosses Rs 40 lakh is required to obtain GST.

Inter-state business: An entity shall register for GST if they supply goods interstate — from one state to another, irrespective of their aggregate turnover. This applies to entities if their annual turnover exceeds Rs 20 lakh. (In special category states, this limit is Rs 10 lakh).

Ecommerce platform: Any individual or entity like Flipkart, Amazon supplying goods or services through an ecommerce platform shall apply for GST registration, irrespective of the turnover.

Casual taxable persons: Any person undertaking the supply of goods, services seasonally or intermittently through a temporary stall or shop must apply for GST irrespective of the annual aggregate turnover.

Voluntary registration: Any entity can obtain GST registration voluntarily. However, after revisions, voluntary GST registration can be surrendered by the applicant at any time.

Special category states: The northeastern states, J&K (erstwhile), Himachal Pradesh, and Uttarakhand.

Filing GST Returns

This is arguably the most important and tedious part of GST from the business/taxpayer perspective. Filing GST returns has become more and more automated. GST returns can be filed online (www.gst.gov.in) using the software or apps provided by Goods and Service Tax Network (GSTN) which will auto-populate the details on each GSTR form.

The following are the GST forms that are to be filed per the rules as of now:

1. GSTR-1 is a detailed report about sales transactions (output) made during a tax period. It also includes reporting any debit and credit notes issued and any changes made to sales invoices. While a normal taxpayer registered under the GST regime should file it monthly, taxpayers whose turnover is up to Rs. 1.5 crore in the previous financial year can file this every quarter.

2. GSTR-2A is a return containing details of all purchases made from registered suppliers during a tax period. This is a read-only return. This data is directly reflected in your report based on the data entered by the registered suppliers in their GSTR-1 return.

3. GSTR-2 is the reporting of all purchases made from registered suppliers during a tax period. The filing of GSTR-2 has been temporarily suspended because GSTR 2A is automatically updated with data from GSTR-1 filed by the suppliers

4. GSTR-3 is a monthly summary return with summarised details about all outward supplies (sales), purchases, input tax credit claimed, along with any tax liability and Taxes paid. This has been temporarily suspended.

5. GSTR-3B This has to be filed by all normal taxpayers registered under GST. It is a monthly self-declaration with summarised details about outward supplies, input tax credit claimed, tax liability and taxes paid.

6. GSTR-4/CMP-08 is the return that the taxpayers have to file every quarter if they have opted for the Composition scheme. CMP-08 is the return that has replaced the former GSTR-4.

7. GSTR-5 is a return that has to be filed by Non-Resident foreign taxpayers who carry out business transactions in India. It is a return to be filed monthly with details about all outward supplies, purchases, input tax credit claimed, along with any tax liability and taxes paid.

8. GSTR-6 is a return that is to be filed monthly by an Input Service Distributor (ISD) - An ISD is a taxpayer who receives invoices for services used by its branches. It contains details about the input tax credit received and distributed by ISD.

9. GSTR-7 is a monthly return to be filed by those who are required to deduct TDS (Tax Deducted at Source) under GST. This will contain details about TDS deducted, TDS liability that is payable/paid and TDS Refund claimed.

As per GST law following people/entities need to deduct TDS :

- A department or establishment of the Central or State Government

- Local authority

- Governmental agencies

- An authority or a board or any other body which has been set up by Parliament or a State Legislature or by a government, with 51% equity ( control) owned by the government

- A society established by the Central or any State Government or a Local Authority and registered under the Societies Registration Act, 1860

- Public sector undertakings

The above deductors are required to TDS where the total value of supply under the contract exceeds Rs 2.5 lakh. The rate for TDS is 2 percent (CGST 1 percent + SGST 1 percent) in case of intrastate supply and 2 percent (IGST) in case of interstate supplies.

10. GSTR-8 E-commerce operators, who are required to collect tax at source (TCS) are to file this monthly. It will contain the details of all the supplies made on the e-commerce platform and the TCS collected.

11. GSTR-9 Taxpayers registered under GST have to file this return annually.

12. GSTR-9A Taxpayers registered under the Composition Scheme have to file this return annually.

13. GSTR-9C is a Reconciliation statement that taxpayers whose turnover is more than Rs 2 crore every financial year have to file.

14. GSTR-10 Any taxpayer whose registered status has been cancelled or surrendered has to file this.

15. GSTR-11 is to be filed by those who have been issued a Unique Identity Number (UIN) to avail refund under GST for the purchase of goods and services in India.

The type of returns that need to be filed varies from business to business.

e-Way Bills and e-Invoicing

Apart from the online filing of the GST returns, the GST regime has introduced several new systems along with it.

e-Way Bills: Under the e-way bill system, manufacturers, traders and transporters can generate e-way bills for the goods transported from the place of origin to their destination on a common portal with ease. Tax authorities are also benefited as this system has reduced time at check -posts and helped reduce tax evasion.

A GST registered person cannot transport goods in a vehicle whose value exceeds Rs. 50,000 (Single Invoice/bill/delivery challan) without an e-way bill that is generated on ewaybillgst.gov.in.

e-Invoicing: The e-invoice system under GST has become mandatory from 1st April 2021 for all registered taxpayers having turnover greater than Rs.50 crore in any financial year from FY 2017-18 onwards.

These businesses must obtain a unique invoice reference number for every business-to-business invoice by uploading it on the GSTN’s invoice registration portal (IRP). The portal verifies the correctness and genuineness of the invoice. Thereafter, it authorises using the digital signature along with a QR code.

e-Invoicing allows interoperability of invoices and helps reduce data entry errors. It is designed to pass the invoice information directly from the IRP to the GST portal and the e-way bill portal. It will, therefore, eliminate the requirement for manual data entry while filing GSTR-1 and helps in the generation of e-way bills too.

Edited by Kanishk Singh

(Disclaimer: The views and opinions expressed in this article are those of the author and do not necessarily reflect the views of YourStory.)

Link : https://yourstory.com/2021/07/understanding-india-indirect-tax-regime-gst-beginners-explainer

Author :- Joseph Varughese ( )

July 04, 2021 at 07:20AM

YourStory