, the food-tech unicorn born in January 2010, will hit the primary market next week with its initial public offering (IPO) to raise Rs 9,375 crore.

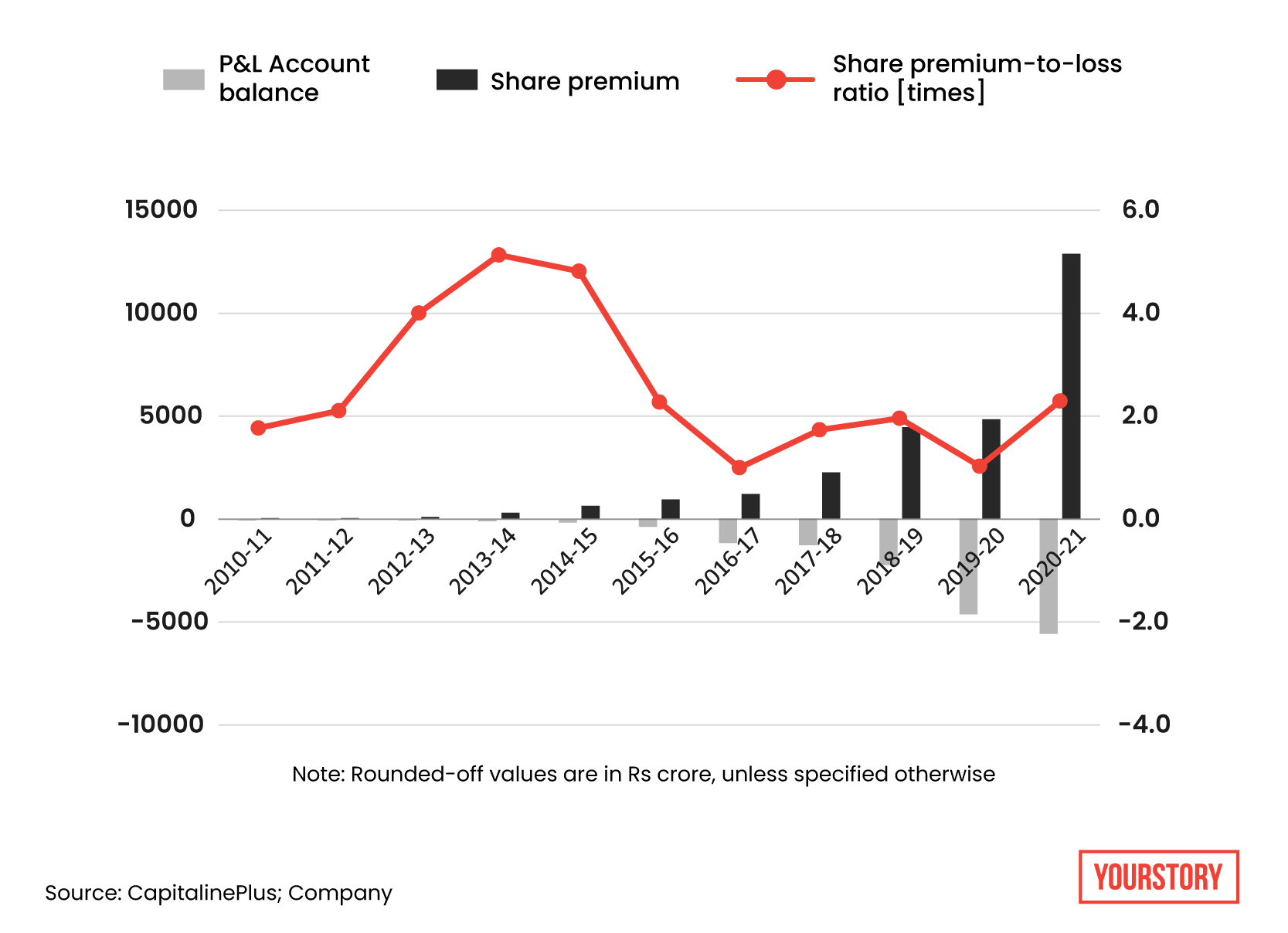

At YourStory, we conducted a detailed analysis of Zomato’s draft red herring prospectus (DRHP) and decoded Zomato’s balance sheets, which have interesting lessons for startup founders. We took the share premium reserve (where the difference between the issue-price and face-value of the issued shares resides), and the loss brought forward every year since 2010-11.

We computed the share premium-to-loss ratio, which implies the notional loss-absorbing capital cushion that Zomato has. The average ratio has been above 2.6 times between 2010-11 and 2020-21.

This capital buffer in the balance sheet gives a budding organisation the confidence to continue its journey towards achieving the desired goal.

In the case of internet businesses like Zomato, the goal is to expand the customer base and market share, which requires continuous cash-burn. And, funds at hand are ideal to keep rather than tapping investors on a need-basis.

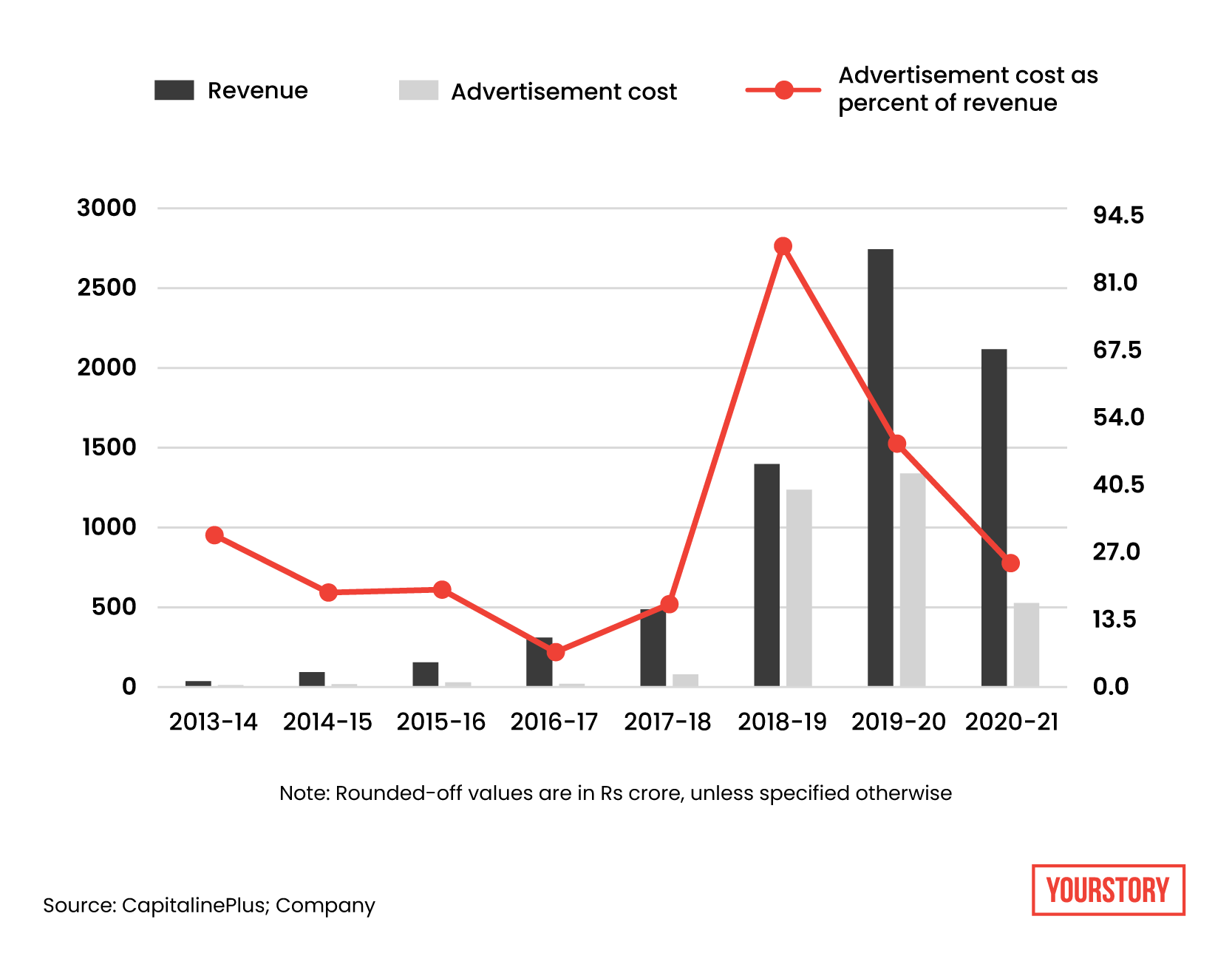

Cash-burn takes us to the advertising costs that Zomato has incurred since 2013-14, and there lies the second lesson for startups. During 2018-19, Zomato’s advertising cost touched Rs 1,236 crore, which accounted for over 88.4 percent of that fiscal’s revenue of Rs 1,398 crore.

Despite having the money to burn, 2019-20 saw an annual increase of 8.3 percent in advertising cost at Rs 1,338 crore, which accounted for 48.8 percent of 2019-20 revenue of Rs 2,743 crore.

Subsequently, in 2020-21, the ratio has again halved to 24.9 percent. The lesson -- do not hesitate to spend if that translates into tangible results. At Zomato, while the advertising cost increased over 2.3 times from 2018-19 to 2019-20, the revenue grew nearly two times in the same period.

But why does Zomato have to keep advertising? With the onset of the pandemic and subsequent lockdowns, the volume of restaurants on its app has been impacted on the supply side.

The number of active food delivery restaurants was 33,192 in 2017-18, 94,286 in 2018-19, 143,089 in 2019-20, and 148,384 in 2020-21.

Just as importantly, on the demand side, Zomato has had to bring back the foodies to the app amidst the pandemic. That’s where advertising is vital. Zomato knows where to find buyers by region, eating, and spending habits because of its experience in using technology to link buyers with restaurants.

And this is how Zomato’s average monthly transacting users stack up: 0.9 million in 2017-18, 5.6 million in 2018-19, 10.7 million in 2019-20, and 6.8 million in 2020-21.

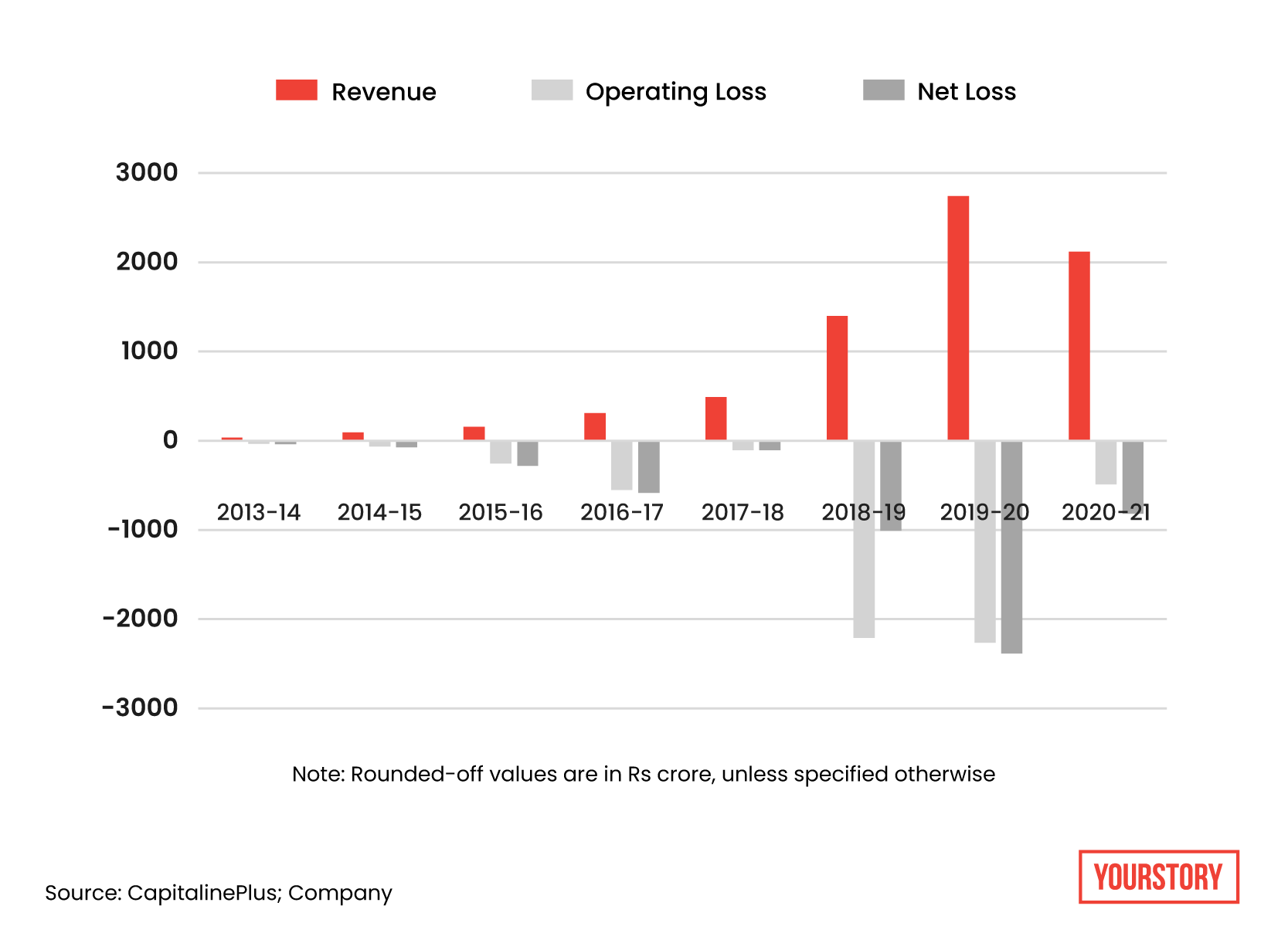

Since 2010-11, Zomato has been a loss-maker in every fiscal, where the net loss has exceeded the revenue by as much as 1.8-1.9 times in 2015-16 and 2016-17, before coming down to 0.2 times in 2017-18.

During 2019-20, at over Rs 2,385 crore, Zomato’s net loss saw a rise of over 2.3 times compared to Rs 1,010-crore loss in 2018-19. Yet, the nearly two times increase in revenue at Rs 2,742 crore in 2019-20 compared to Rs 1,397 crore in 2018-19 points at Zomato’s frugal operation in a highly competitive market.

Zomato’s 2020-21 performance amplifies the frugality view, because despite a decline in revenue by Rs 624 crore, or 22.8 percent, to Rs 2,118 crore, its loss reduced heavily by Rs 1,569 crore to over Rs 816 crore.

For investors at large, the loss-making nature of internet businesses deserve to be given lesser weightage when there is exponential growth in transacting user bases. And Zomato has experienced rapid growth in food delivery orders which increased 13.2 times from 30.6 million in 2017-18 to 403.1 million in 2019-20, while its gross order value (GOV) grew 8.4 times from Rs 1,334 crore to Rs 11,220 crore in the above period.

The pandemic challenges reflect in Zomato’s 2020-21 numbers as orders values dipped to 238.9 million while the GOV came down to over Rs 9,482 crore.

While the IPO values Zomato at Rs 64,365 crore, it plans to utilise a sizeable portion of the fundraise to pursue organic and inorganic growth opportunities. Its early 2020 acquisition of Uber Eats through a share-swap deal valued, estimated by YourStory at nearly Rs 1,376 crore, was aimed at acquiring Uber Eat’s customer base and gaining market share.

Through its current journey to the primary market, Zomato joins the internet business’ club of Delhi, like Info Edge (India), MakeMyTrip, and IndiaMART InterMESH that have successfully listed publicly.

Investor interests

The other important feature of the IPO is that just Rs 375 crore worth of shares will be tendered by Info Edge (India) – Zomato’s early backer, which runs Naukri.com among other online businesses through offer for sale (OFS) route.

In late April, Info Edge’s board had resolved to use the OFS route to garner Rs 750 crore. For investors evaluating Zomato’s IPO from the fence, Info Edge’s opting to trim the OFS portion by half indicates that it sees a lot of steam left in Zomato even after the IPO.

The YourStory analysis also reveals that China’s Alibaba Group, through group entities Alipay Singapore Holding and Antfin Singapore Holding, had invested over Rs 2,862 crore in three tranches; February and November 2018, and January 2020. Similarly, Tiger Global has invested over Rs 1,887 crore in Zomato through Internet Fund VI in three tranches; September and December 2020, and February 2021.

Overall, the cash consideration for convertible preference shares, paid by various investors including Mirae, Kora, Fidelity, among other marquee names, crossed a whopping Rs 11,302 crore during March 2012 to February 2021. And, none of the existing investors, except Info Edge are using the IPO for an exit.

That financial investors are not using the IPO to exit, gives a strong reason to believe that the food-tech unicorn is being seen as an investment that could provide a lot more upside in the future.

Link : https://yourstory.com/2021/07/frugality-lessons-zomato-unicorn-ipo

Author :- Rajiv Bhuva ( )

July 09, 2021 at 12:23PM

YourStory