Two seasoned bankers with over 25 years of experience felt the existing banking infrastructure in the country has not reached out to those who really need credit, and decided to take the entrepreneurial route to address this gap.

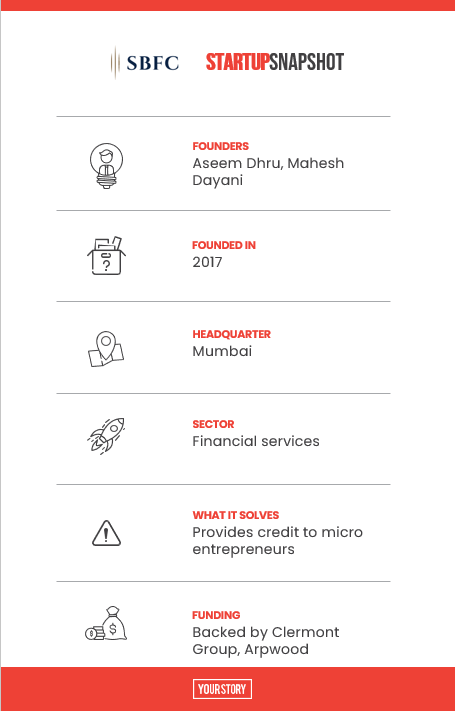

To provide credit to those sections of the society who normally would not qualify for a bank loan, Aseem Dhru and Mahesh Dayani founded SBFC Finance, a non-banking finance company (NBFC) in September 2017.

“The banks, both public and private sector, cater to a segment of customers who have the requisite credit scores and regular incomes, and usually do not service thin-file customers. With incremental new borrowers in emerging towns and cities, the credit from the organised lenders is not apt,” says Aseem, who has previously worked with HDFC Bank.

Diversity

The diversity of the country itself creates various kinds of borrowers, but the financial institutions have not been able to create the infrastructure or have the know-how to deal with this segment as they typically do not have conventional credit score information.

“In India, there are 65 million small businesses across the country, and not more than 8-9 percent of them have any form of organised finance. They largely borrow from unorganised sources or from friends and family or trade credit and all this comes at an expensive price,” says Mahesh, who also has over 25 years of banking experience with Kotak Mahindra Bank.

The startup is looking to replace this unorganised borrowing with organised finance at affordable rates and it believes this gap is a huge opportunity.

Types of loans

SBFC Finance offers a mix of secured and unsecured loans. These include secured loans for micro-enterprises to meet working capital and term loan requirements. These are served to MSMEs and self-employed non-professionals with collaterals.

The NBFC also provides loans against gold and also small ticket personal loans, which are unsecured. There are also business and professional loans, which are unsecured and short-term in nature.

“Our loans help customers launch businesses, open premises, hire more people, upgrade equipment, develop products, and do the other things needed to grow and prosper,” says Mahesh.

Besides this, the startup also offers a full suite of specialist Loan Management Services, helping institutional lenders to manage all aspects of loan servicing, including client relations, collections, payments, porting, and data storage.

It manages LMS for institutions such as the State Bank of India, IndusInd Bank, Avenue Capital, Nippon AMC, SSG, and Dewan Housing Finance Corporation (DHFL).

Aseem says, “This innovative offering bolsters our fee income, without any risk on our books, and strengthens our position as a niche industry player.”

Omnichannel model

The services and products of SBFC Finance are delivered through an omnichannel model, which is a combination of branch and digital channels.

According to Aseem, the direct connect and local presence through a hub-and-spoke model provides them with valuable customer insights about these underserved markets.

Today, SBFC Finance is present in 17 states and 100 cities and says it is lending at a nominal rate, where the focus is to provide the right credit to the right customers.

“We have overcome language barriers and property issues and have built a robust credit rule engine, which results in profitability at unit economics. Once you get it right in the beginning of the journey, it keeps on snowballing,” says Aseem.

SBFC Finance currently has a loan book of around Rs 3,700 crore and is projected to achieve a net profit of Rs 100 crore for FY21. It disburses more than Rs 100 crore on a monthly basis.

“Our prudent strategies and focus on driving profitable growth have helped strengthen our profitability quotient. From growth capital to overall profitability and asset quality, we have sustained healthy financials,” says Mahesh.

SBFC Finance is backed by Singapore-based Clermont Group and Arpwood with an equity infusion of Rs 845 crore, who have been with the NBFC since inception. It is also capitalised at almost of Rs 1,000 crore.

Understanding customers

Financing small businesses come with its own challenges around documentation, unpredictable cashflows, and so on. “At SBFC, we have put in place a robust and scalable business model to overcome these challenges and cater to the growing financial appetite of these customers,” says Aseem.

He further elaborates that the expansive presence of SBFC Finance with in-depth local insight and relationships with borrowers has helped to bring more people into the formal banking ambit.

There are also other established NBFCs like Bajaj Finance and Shriram Finance who operate in a similar segment, and there are also new-age startups Lendingkart, MoneyTap, etc.

SBFC has lined up an ambitious expansion plan in terms of distribution and scale, which will mean the addition of infrastructure, human, and financial capital. “This will result in a disbursement increase by 15 percent every quarter for the next 12-18months,” says Aseem.

The team at SBFC Finance

The plan is to be present in one-third of the districts in each of the states where it is present. To keep the risk distributed, SBFC Finance ensures that each state does not have a book size, which is more than 20 percent.

The future certainly looks bright for SBFC Finance as it makes deep inroads into the market to onboard people onto the mainstream, giving a boost to financial inclusion. At the same time, there is a strong focus on the business metrics.

“Our strong profitable growth in the past three years bears testimony to our ability to design and launch products that meet diverse needs without compromising on asset quality,” says Mahesh.

Edited by Megha Reddy

Link : https://yourstory.com/2021/06/sbfc-finance-nbfc-startup-financial-inclusion

Author :- Thimmaya Poojary ( )

June 22, 2021 at 06:00AM

YourStory